The recent gains are a rare sight in 2023, even considering Bitcoin’s impressive 108% year-to-date performance. Notably, the last instance of such price action occurred on March 14 when Bitcoin surged from $20,750 to $26,000 in just two days, marking a 25.2% price increase.

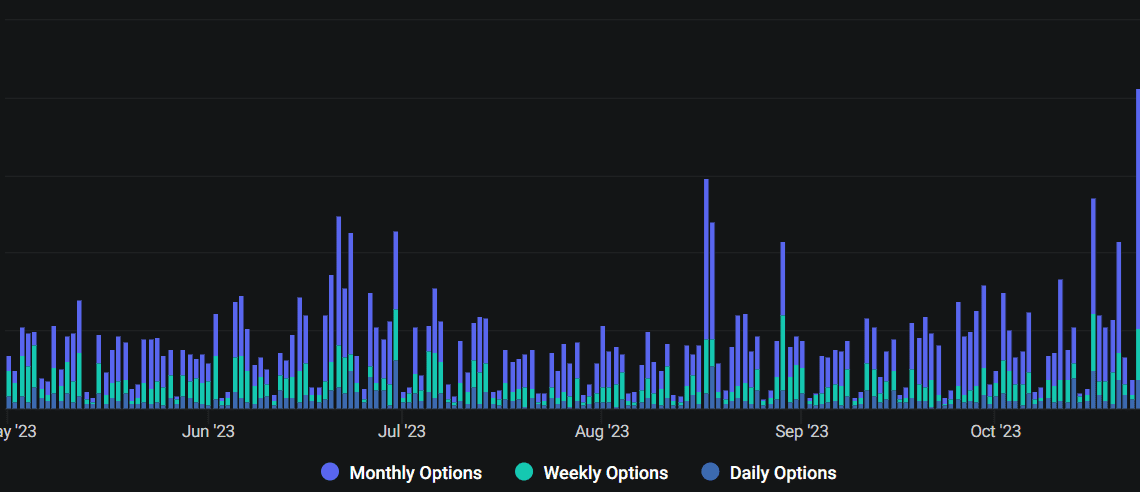

It’s worth noting the significance of the fact that a staggering 208,000 contracts changed hands in a mere two days. To put this into perspective, the prior peak, which occurred on August 18, saw a total of 132,000 contracts exchanged, but that was during a period when Bitcoin’s price plummeted by 10.7% from $29,090 to $25,980 in just two days. Interestingly, Bitcoin’s options open interest, which measures outstanding contracts for every expiry, reached its highest level in over 12 months on Oct. 26.

This surge in activity has led some analysts to emphasize the potential “gamma squeeze” risk. This theoretical analysis seeks to capture the need for option market makers to cover their risk based on their likely exposure.

the #bitcoin gamma squeeze from last week could happen again

if BTCUSD moves higher to $35,750-36k, options dealers will need to buy $20m in spot BTC for every 1% upside move, which could cause explosiveness if we begin to move up towards those levels

more pic.twitter.com/OA9tJ0ZaK9

— Alex Thorn (@intangiblecoins) October 30, 2023

According to estimates from Galaxy Research and Amberdata, BTC options market makers may need to cover $40 million for every 2% positive move in Bitcoin’s spot price. While this number may seem substantial, it pales in comparison to Bitcoin’s staggering daily adjusted volume of $7.8 billion.

Another aspect to consider when assessing Bitcoin options volume and total open interest is whether these instruments have primarily been used for hedging purposes or neutral-to-bullish strategies. To address this ambiguity, one should closely monitor the demand difference between call (buy) and put (sell) options.

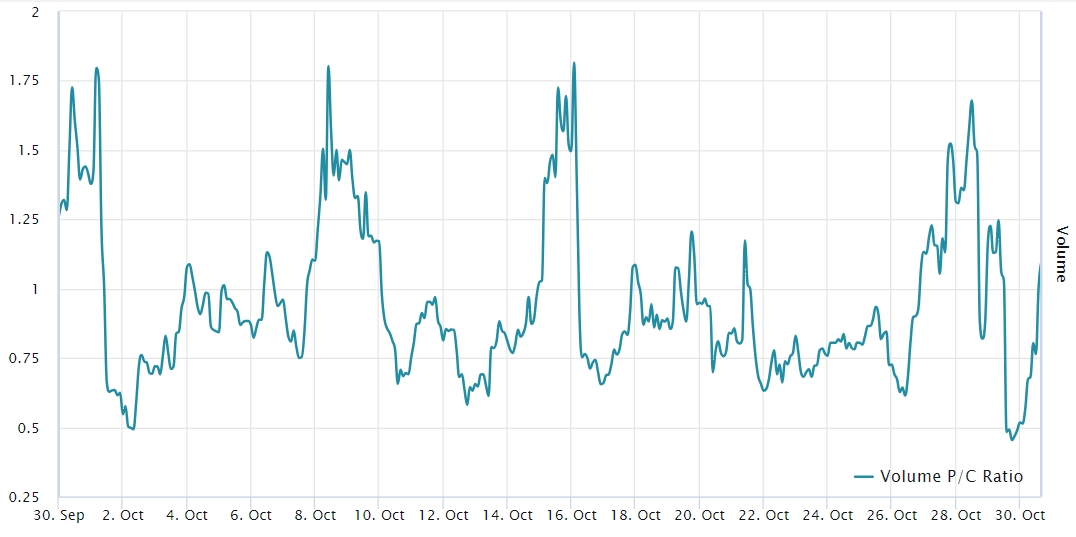

Notably, the period from Oct. 16 to Oct. 26 saw a predominance of neutral-to-bullish call options, with the ratio consistently remaining below 1. Consequently, the excessive volume observed on Oct. 23 and 24 was skewed towards call options.

However, the landscape changed as investors increasingly sought protective put options, reaching a peak of 68% higher demand on Oct. 28. More recently, the metric shifted to a neutral 1.10…

Click Here to Read the Full Original Article at Cointelegraph.com News…