Asset tokenization is one of the more compelling concepts in the current blockchain development cycle. Dacoinmister’s Second Bitcoin Whitepaper (proposing to build MasterCoin on top of the Bitcoin network) first described it in 2012. In 2014, Tether launched as the first tokenized fiat “stablecoin.”

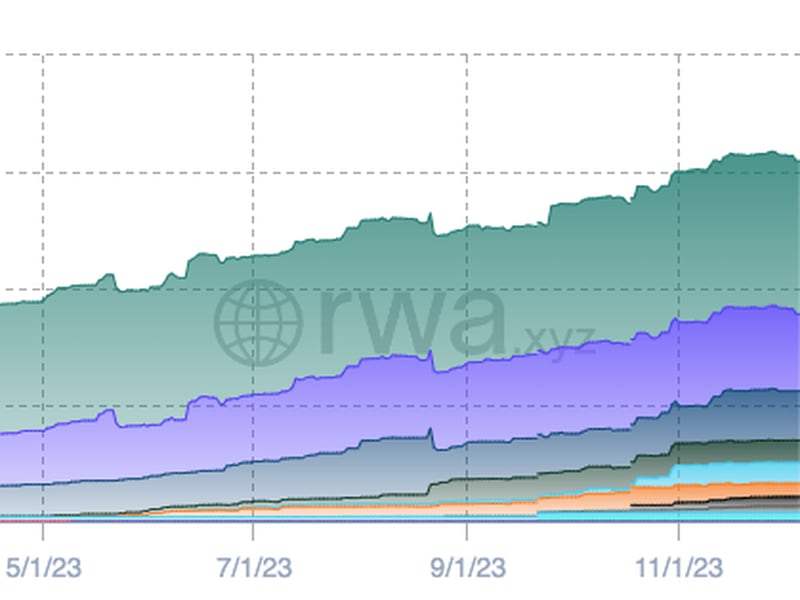

The overall market capitalization of tokenized assets has now surpassed $200B, with $128 billion in stablecoins and $1.3 billion in other real world assets (RWAs) including U.S. Treasuries, real estate and debt.

You’re reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

Source: https://app.rwa.xyz/treasuries

With increased institutional interest in crypto on the horizon, we expect tokenization to continue growing exponentially in 2024. With that in mind, this article introduces a new concept that could amplify tokenization’s growth: TaxWraps.

To understand TaxWraps, let’s explore dividend taxation. When companies pay out profits as non-qualified dividends, recipients face immediate tax liabilities. ETFs (exchange-traded funds) are one tool to defer tax obligations. ETFs often reinvest dividends back into the fund, allowing value to grow tax-deferred until investors sell their ETF shares. This allows investors to defer tax obligations while compounding their wealth. With TaxWraps, our goal is to broaden the ETF-style deferral mechanism via tokenization.

Consider a tokenized asset fund or trust (TAFs). A family office wishing to minimize their tax burden can perform in-kind transfers of income-generating stocks/assets to TAFs and, in return, receive tokens representing their ownership in the trust. Like ETFs, these tokens derive their value from the pool of assets in the fund.

When the stocks/assets generate income, the fund will acquire more of the underlying asset (e.g. reinvesting the dividends) and the existing token pool’s value will increase. When the family office is ready to liquidate its holdings, tokens can either be sold or burned, at which point only the overall gains or losses are considered for tax purposes.

Without getting into the complexities of tax codes and appropriate structuring of the TAFs, this simplified model could act as a beacon of tax…

Click Here to Read the Full Original Article at Cryptocurrencies Feed…