One of the laziest and most frustrating criticisms of digital currencies — particularly Bitcoin (BTC) — is when pundits liken it to a pyramid scheme dependent on the “greater fool” joining to make a quick buck. While some people do indeed purchase digital assets purely for speculative purposes, it’s unfair to ignore many of the great services and achievements that are being made by developers in areas such as remittances, logistics, financial inclusion and intellectual property.

A fairer criticism of blockchains is that, for all proponents say about decentralization, blockchains are still dependent on miners or other powerful players that control their networks. Whether it be factories filled with servers for proof-of-work (PoW), pools of PoW miners, large pools of tokens for proof-of-stake (PoS), or the fact that at times, more than 50% of transactions that run on the Ethereum network run through the Infura API, there’s no ignoring these massive centralized points of failure.

Granted, the design of popular PoW and PoS blockchains has been incentivized to ensure bad actors are punished, yet it remains to be seen how they will operate when the value of digital assets operating on certain blockchains exceeds the value of the underlying ledger’s native coin.

Related: Ethereum’s Merge will affect more than just its blockchain

Imagine, for instance, if a popular stablecoin grew so large that its total value exceeded that of the native coin of the underlying blockchain it operated on. Essentially, it would create an inverse pyramid whereby the holders of the native token could control the transactions of the said stablecoin. Given the concentration of many crypto assets among “whales” who have a vested interest in their blockchain’s native token (and price), this could become a very real problem.

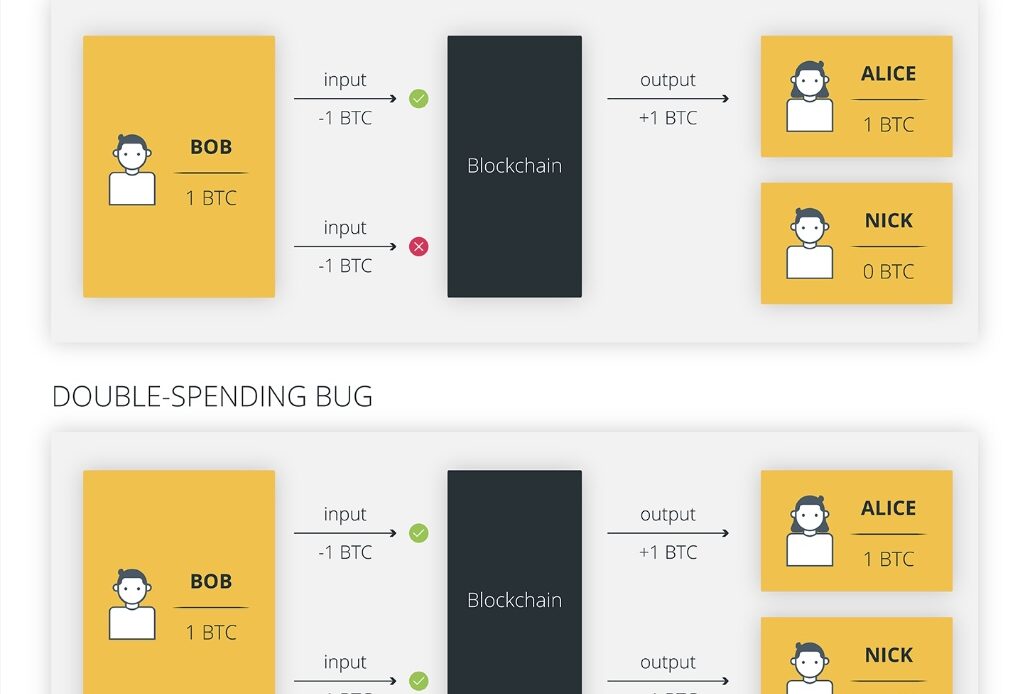

In Ethereum, as a PoS ledger, miners’ stakes are in Ether (ETH). Should Tether (USDT) or USD Coin (USDC) become larger than Ether in market value, they could theoretically pull off a double-spend in those respective digital currencies, lose their Ether stake, and still profit more from the double-spend. Although it still remains hypothetical, it’s by no means unimaginable.

This then poses a question regarding how we should rethink distributed ledger technology (DLT) architecture and the role mining or staking assets should play.

Tether now boasts a market capitalization of over $80 billion, Circle just under $30 billion, while the Ethereum…

Click Here to Read the Full Original Article at Cointelegraph.com News…