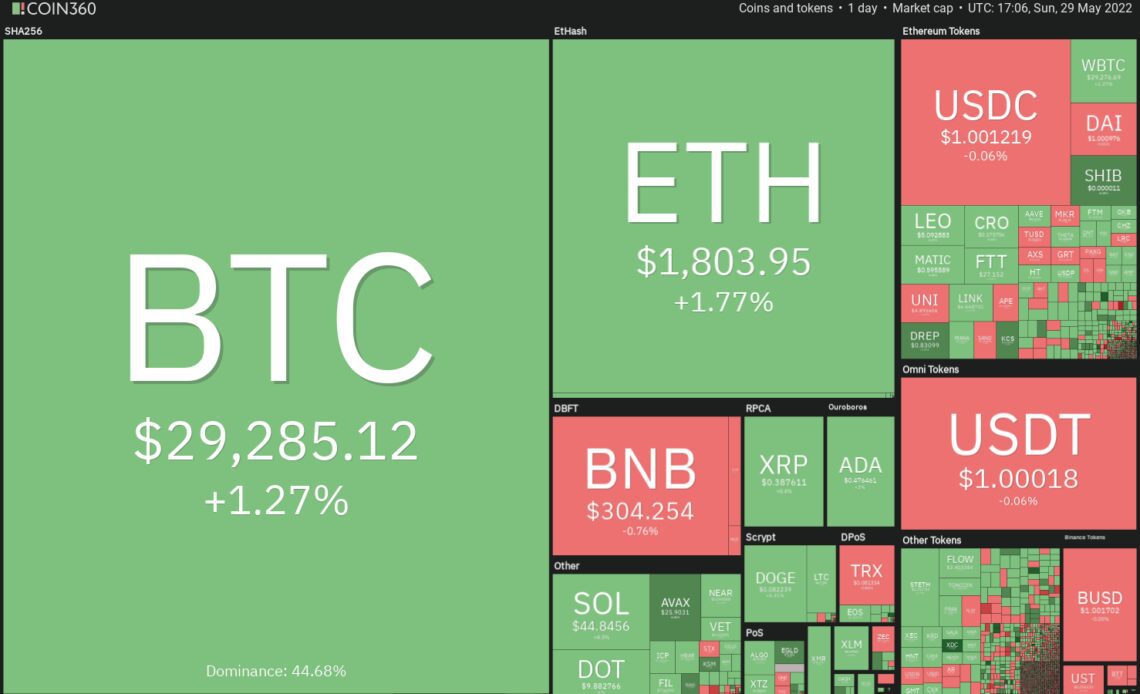

After declining for eight successive weeks, the Dow Jones Industrial Average rebounded sharply last week to finish higher by 6.2%. However, Bitcoin (BTC) has not been able to replicate the performance of the United States equities markets and is threatening to paint a red candle for the ninth week in a row.

A positive sign is that Bitcoin whales have been buying the market correction. Glassnode data shows that the number of Bitcoin whale wallets with a balance of 10,000 Bitcoin or more has risen to its highest level since February 2021. The accumulation in the whale wallets suggests that their long-term view for Bitcoin remains bullish.

Blockware Solutions highlighted that the Mayer Multiple metric which compares the 200-day simple moving average with the current price was languishing “near some of the lowest readings on record.” The firm said a few other indicators also suggest that Bitcoin is attempting to form a bottom.

If Bitcoin starts a recovery in the short term, certain altcoins are likely to follow it higher. Let’s study the charts of the top-5 cryptocurrencies that may lead the relief rally.

BTC/USDT

Bitcoin remains stuck inside a tight range between the downtrend line and the support at $28,630. The bears pulled the price below $28,630 on May 26 and May 27 but could not sustain the lower levels. This resulted in a rebound on May 28.

The bulls will now try to push the price above the downtrend line and challenge the 20-day exponential moving average ($30,538). If they succeed, the BTC/USDT pair could pick up momentum and the rally could reach the 50-day SMA ($35,181).

The positive divergence on the relative strength index (RSI) suggests that the bearish momentum could be weakening and a rally may be around the corner.

On the other hand, if the price turns down from the overhead resistance, the bears will again try to pull the pair below $28,630. If they manage to do…

Click Here to Read the Full Original Article at Cointelegraph.com News…