Data shows Bitcoin has been more stable than gold, DXY, Nasdaq, and S&P 500 recently, here’s what history says could follow next.

Bitcoin 5-Day Volatility Has Fallen Below That Of Gold, DXY, Nasdaq, And S&P 500

According to the latest weekly report from Arcane Research, BTC has been more stable than these assets for a record duration already this year. The “volatility” is an indicator that measures the deviation of daily returns from the average for Bitcoin.

When the value of this metric is high, it means the crypto has been registering a higher amount of returns compared to the mean, suggesting that the coin has involved a higher trading risk recently. On the other hand, low values imply there haven’t been any significant fluctuations in the price in recent days, showing that the market has been stale.

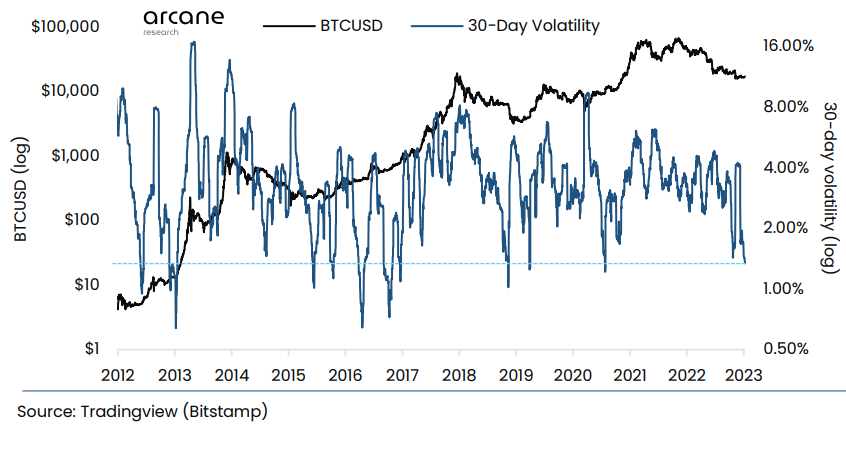

Now, here is a chart that shows the trend in the 30-day volatility for Bitcoin over the course of its entire history:

The value of the metric seems to have plunged in recent days | Source: Arcane Research's Ahead of the Curve - January 10

As shown in the above graph, the Bitcoin 30-day volatility is at very low levels currently as the price has been trading mostly sideways in recent weeks. The current values of the indicator are the lowest since 2020, but they are still higher than some of the lows during previous bear markets.

One consequence of this recent flat movement has been that BTC has become more stable than assets like gold, DXY, Nasdaq, and S&P 500. To compare these assets’ volatilities against each other, the report has made use of the 5-day volatility (and not the 30-day or 7-day one).

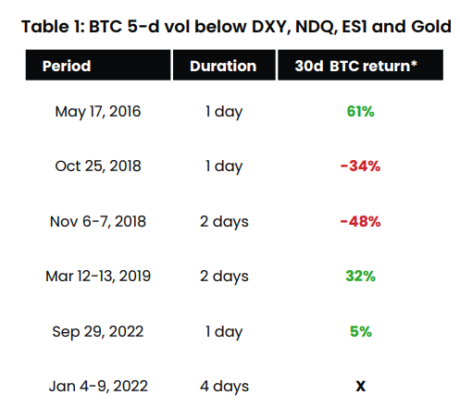

The below table highlights the periods in BTC’s lifetime when the crypto’s 5-day volatility has been simultaneously lower than all these traditional assets.

Looks like such occurrences have been a very rare event | Source: Arcane Research's Ahead of the Curve - January 10

As the table displays, there have only ever been a handful of instances where the Bitcoin 5-day volatility has been lower than that of gold, DXY, Nasdaq, and S&P 500 at the same time. The report labels such occurrences as “relative volatility compression” periods.

It seems like, before the latest streak, the highest duration of this trend was just 2 consecutive days. This means that the current relative volatility compression period is already the longest ever in the coin’s history.

Another interesting fact in the table is the total returns in Bitcoin that were…

Click Here to Read the Full Original Article at NewsBTC…